We use cookies to give you the best digital experience. By continuing to browse this site, you give consent for cookies to be used. To learn more information about the use of cookies, please visit our cookie policy.

China's beauty market has always rewarded brands that move fast. But in 2026, speed alone is no longer enough. The rules of engagement have changed — and for international beauty brands, the shift is more fundamental than a product reformulation or a new KOL roster. Chinese consumers have quietly redrawn the purchase decision from "which product performs best" to "which brand understands me." That distinction is the difference between growing and losing ground in the world's largest cosmetics market.

This article unpacks four Chinese beauty trends in 2026 that every international CMO should have in their strategy brief. It translateseach into a platform-level action for Xiaohongshu, Douyin, and Tmall.

The Market Reset: Recovery Is Real, But the Rules Have Changed

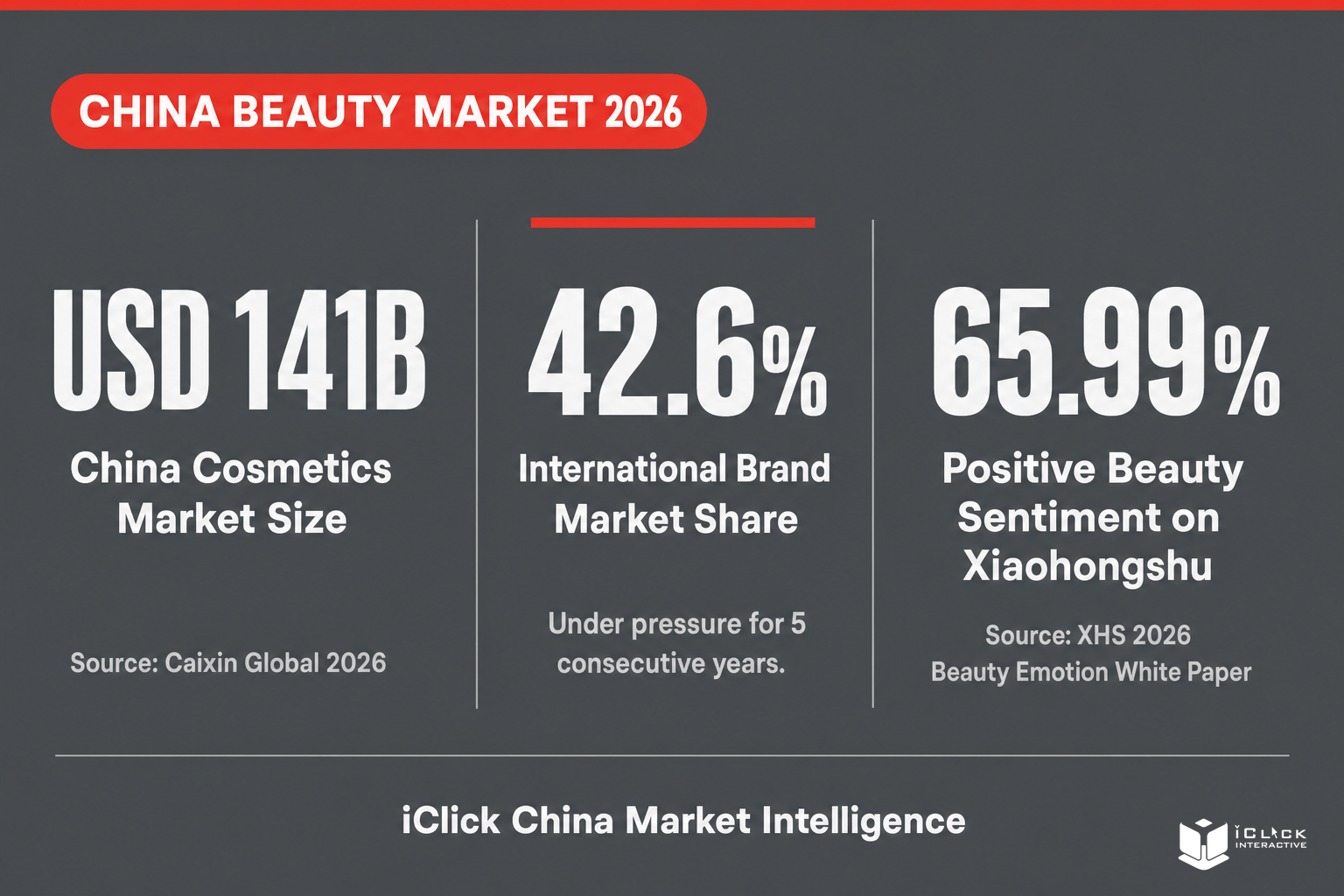

China's cosmetics market reached approximately USD 141 billion (RMB 1.1 trillion) in 2025, with online channels accounting for 65.4% of all transactions. The first half of 2025 saw sales grow 2.9% year-on-year to USD 32.5 billion, a genuine recovery signal after two years of cautious consumer sentiment. But this is a quality-led recovery, not a volume-led one. Shoppers are buying less and spending more deliberately.

For international brands, the structural challenge is sharper than the headline growth suggests. Homegrown Chinese beauty labels — collectively known as C-Beauty — now hold 57.4% of the market, their fifth consecutive year of share gains. French brands remain the strongest foreign bloc at 16.1%, followed by US brands at 11.7%, Japanese brands at 6.4%, and Korean brands at 4%.

What is C-Beauty? C-Beauty refers to a new generation of homegrown Chinese cosmetics brands, including Florasis (花西子), Proya, Winona, and Maogeping, that have rapidly moved into the premium tier. Their edge is structural: ingredient storytelling rooted in Traditional Chinese Medicine, agile supply chains that compress time-to-market to weeks, and deep native fluency on Xiaohongshu and Douyin. International brands are not losing to C-Beauty on price, they are losing on emotional relevance and platform velocity.

On the channel side, Douyin has overtaken Tmall as the primary GMV driver for beauty, and fragrance has emerged as the single fastest-growing sub-category across both platforms.

Trend 1: Beauty in Moods — Emotional Efficacy Is the New Performance Claim

The most significant strategic signal for 2026 comes from Xiaohongshu's own data. The platform's 2026 Beauty Emotion White Paper analyzed more than 200,000 beauty-related notes across 95 distinct emotion categories. The findings reframe what Chinese consumers are actually buying.

66% of beauty conversations on Xiaohongshu carry positive emotional sentiment. The standout emotion is appreciation, which indexes at 26.43% inside beauty content, versus 10.27% across the broader platform. Beauty also generates disproportionate acceptance signals (3.55% vs. 1.26% market-wide), suggesting that consumers use beauty purchases to affirm identity, not just to address a skin concern.

The strategic implication for international beauty brand marketers:

The creative brief has to change. Leading with ingredient efficacy — "3% retinol," "10 clinical trials," "dermatologist recommended" — answers the wrong question at the wrong moment. On Xiaohongshu, the first touchpoint is emotional seeding, not functional proof. Premium positioning works best when the emotional promise centers on reassurance and composure. Mass-market positioning should lean into accessibility and immediacy.

Xiaohongshu's paper also identifies three gifting occasions that drive purchase: self-gifting (personal reward), intimate gifting (relationship expression), and outward gifting (social visibility). Each requires a distinct content and CTA strategy.

Action for Marketers:

Rebuild Xiaohongshu seeding briefs around mood occasions. "Post-work reset ritual" and "Sunday skin ceremony" outperform "best moisturizer for dry skin" in discovery-stage content. Map each SKU to one of the three gifting modes and build distinct creative tracks for each.

Trend 2: Biotech and Clinical Proof — The Only Defensible Moat

While emotional fit wins on Xiaohongshu, purchase decisions on Tmall and JD are increasingly anchored in scientific credibility. The prestige tier in 2026 is dominated by clinically validated serums, barrier-repair treatments, and derm-device hybrids. Consumers want proof, before-and-after results, credible education, and visible ingredient transparency.

This trend matters because C-Beauty has closed the R&D gap faster than most international brands anticipated. Listed domestic cosmetics firms now allocate 3.24% of revenue to R&D, a share that has grown steadily year-on-year. The "cheap local alternative" narrative is obsolete. International brands can no longer win on heritage brand equity alone; they need to demonstrate scientific superiority at the product-detail page level.

Two adjacent trends amplify this: scenario skin (consumers adopting skin-focused routines across categories previously unassociated with skincare, such as makeup and body care) and skinification (applying skincare-grade actives to hair, scalp, and lip products). Both create white space for internationally recognized dermatological and pharmaceutical parent companies to extend credibility into new formats.

Action for Marketers:

Lead Tmall and JD PDPs with clinical data, third-party certifications, and dermatologist endorsements. Reserve emotional brand narrative for Xiaohongshu seeding. Run the two in sequence — emotion discovers, science converts.

Trend 3: Wellness Crossover — Beauty Is Now a Health Category

The fastest-growing expressions of this are scalp care (driven by stress-related hair loss discussions on Xiaohongshu), oral beauty (teeth whitening, gum care, and breath wellness), UV and outdoor-performance products (linked to the growing outdoor sports culture documented in our Spring Fashion 2026 analysis), and what Florasis CMO Gabby Chen has described as "emotional efficacy" — beauty routines designed from scent to texture to packaging to soothe and restore, not just treat.

For international brands with pharmaceutical or dermatological parent companies, this convergence is a significant positioning opportunity that local competitors cannot easily replicate.

Action for Marketers:

Identify SKUs that bridge beauty and wellness. Brief Douyin content creators to produce short-form videos that lead with the wellness angle: sleep, stress recovery, and scalp health, rather than the cosmetic outcome. This unlocks health-content audiences in addition to beauty audiences.

Trend 4: Pan-Fragrance — The White Space International Heritage Brands Can Still Own

Fragrance is China's fastest-growing beauty segment, and it remains the category where international heritage houses hold the clearest advantage. C-Beauty players, including Maogeping, Songmont, and concept stores like LaPorte, are entering the fragrance space and building new olfactive narratives. But the category is still underpenetrated relative to Western markets, and heritage olfactive storytelling is a structural asset that takes decades to build.

The 2026 opportunity is a pan-fragrance portfolio approach: anchored EDP and EDT lines extending into body mist, hair perfume, home fragrance, and emerging neuro-scent formats (functional fragrances positioned around focus, calm, or energy). Each extension creates a new entry price point, a new gifting occasion, and a new Xiaohongshu content vertical.

Action for Marketers:

Map your fragrance IP across the full scent-occasion spectrum before C-Beauty players lock in the emerging categories. Invest in offline sampling at high-footfall retail destinations — fragrance conversion on Douyin live streams is lower than for skincare because scent requires a physical first encounter. Treat Xiaohongshu as the discovery layer; treat offline as the trial layer; treat Douyin live as the repurchase layer.

The 2026 Playbook:

Consumer Shift → Platform Behavior → Brand Action

| Consumer shift | Platform behavior | International brand action |

| "What fits me" over "what works" | Xiaohongshu emotion-tagged seeding | Rebrief creative around mood occasions and gifting modes |

| Multi-factor decision beyond price | Tmall / JD PDP clinical validation | Front-load efficacy data and derm endorsements |

| Beauty = wellness lifestyle | Douyin health-beauty crossover content | Build a dual wellness + beauty content funnel |

| Scent as an emotional anchor | Xiaohongshu scent notes + Douyin live repurchase | Pan-fragrance portfolio + offline trial activation |

The brands that will gain ground in China in 2026 are not the ones with the largest media budget — they are the ones that understand which platform earns trust, which earns trial, and which earns conversion, and that build their strategy accordingly.

Partner with iClick to translate these four shifts into a winning Chinese media strategy that protects your share against C-Beauty — and opens new category white space before local competitors do.

Data and insights referenced in this article are drawn from the following sources:

- Xiaohongshu 2026 Beauty Emotion White Paper — emotional sentiment distribution, appreciation index, gifting occasion taxonomy

- Caixin Global, "China's Homegrown Cosmetics Brands Now Dominate World's Largest Beauty Market" (January 2026) — market size (USD 141B), domestic vs. international brand share, online channel share (65.4%)

- BeautyMatter, "China Beauty Predictions for 2026" — clinical-grade skincare trend, wellness crossover, emotional efficacy, H1 2025 sales data

- Jing Daily, "China's 2026 Beauty Trends: Scenario Skin, Neuro-Scent and Biotech" — scenario skin, skinification, pan-fragrance, biotech-led innovation

- Daxue Consulting, "2026 China Beauty Trends Report" — category and consumer behavior overview

- Cosmetics Business, "China's Beauty Market Is Bouncing Back in 2026" — market recovery context

- PCHi 2026 — sensory experience and efficacy-led innovation signals

Related Insights: Explore More on China's Beauty and Digital Media Landscape

🔗 Beyond the Lipstick Effect: Navigating China's 'Perfume Effect' Era: China's USD 6.8 billion fragrance market is evolving fast — and for international brands, it represents one of the last high-growth categories where heritage storytelling still wins. Discover how Gen Z and Millennials are choosing scents based on emotional preference over price, and how Le Labo and Byredo are capitalizing on China's perfume boom through culturally resonant digital strategies on Xiaohongshu and Douyin.

🔗 Chinese Media Insight Spotlight #22 – May Media Updates Stay ahead of the platform shifts that directly impact your China beauty strategy. This edition covers Xiaohongshu's Brand Zone expansion (keyword capacity up from 30 to 300), Fliggy's 88VIP member growth at 40% and 10% higher repurchase rate, and Tencent's new ad compliance frameworks — essential reading for CMOs managing full-funnel campaigns across China's key digital platforms.

🔗 What is Influencer Marketing: Your Comprehensive Guide: Building a Xiaohongshu seeding program or Douyin KOL strategy starts with the right structural foundation. This guide covers influencer tiers from nano to mega, campaign formats, platform selection, and ROI measurement — with an average USD 6.50 return per USD 1 invested as the benchmark — equipping beauty marketing teams to build data-driven influencer programmes that deliver measurable growth.